Remarks by leaders from Maruti Suzuki, Axis-linked insurance, Pay10 and Luminous highlighted how mobility readiness, regulatory reform and financial sovereignty are diverging across sectors

EV Hesitation, Solar Confidence and UPI’s Global Test Shape India’s Economic Debate in Delhi

India’s economic conversation is no longer moving in a single direction. Instead, it is unfolding through sector specific realities that reveal differing levels of readiness, confidence, and constraint. This divergence was clearly visible during discussions in New Delhi where senior leaders from automobiles, insurance, payments, and energy reflected on how India’s geoeconomic position is being shaped in practice, not theory.

Banerjee pointed to range anxiety, charging access, and ownership experience as unresolved issues for the company’s core customer base. Rather than chasing early adopters, he said the focus remains on resolving practical barriers before introducing the e-Vitara electric SUV. Maruti Suzuki has already established over 2,000 dedicated EV charging points across more than 1,100 cities and partnered with 13 charge point operators, with an ambition to scale the charging ecosystem to one lakh chargers nationwide by 2030. The approach reflects a broader view that sustainable mobility must align with consumer readiness and infrastructure depth, not just product availability.

Bajaj also addressed the evolving conversation around energy storage, noting that reliance on a single battery technology such as lithium ion presents both vulnerabilities and opportunities. She suggested that India’s strength lies in layering its software and engineering capabilities across multiple storage solutions, adapting technologies to local power conditions rather than following a uniform global template. The emphasis was on pragmatic innovation, shaped by domestic demand rather than first mover advantage.

Madan also pointed to the removal of GST on life insurance as a meaningful signal. Demand, he said, has already shown signs of picking up following the tax relief, reinforcing the view that policy design plays a decisive role in shaping consumer behaviour. At the same time, he stressed that insurers themselves carry responsibility in communicating value and building trust, especially as the sector moves toward a more customer centric framework.

Gill explained that many countries are strengthening their domestic payment ecosystems, often with high capital and localisation requirements. Recent changes by the Reserve Bank of India around aggregate cross border licences, he said, are enabling Indian firms, particularly small and medium enterprises, to explore international markets with greater confidence. However, he emphasised that global adoption of UPI will depend on whether it delivers tangible value to merchants abroad, including faster settlements and competitive pricing compared to established card networks.

You may also like

Lenspoke has introduced Kerala's first ZEISS VISION CENTER in Kochi, offering advanced eye diagnostics, personalised consultations and premium optical...

More than 50,000 students across IITs, IIMs, NITs and leading universities participated in Vande Bharatam's nationwide campus outreach, reflecting growing...

Recognition for all three Sterlite Group companies in India's Best Workplaces 2026 reflects a shared focus on workplace culture, employee experience and...

A sharp rise in Products segment revenue helped Umiya Buildcon deliver a steady first quarter performance, while continued investments in networking...

The agreement connects an Indian green methanol project with an international buyer and places Odisha within a growing supply network for cleaner marine fuels...

MG Group has introduced Starz, its next-generation premium coach platform, at Prawaas 2026, marking a significant addition to India's passenger mobility sector...

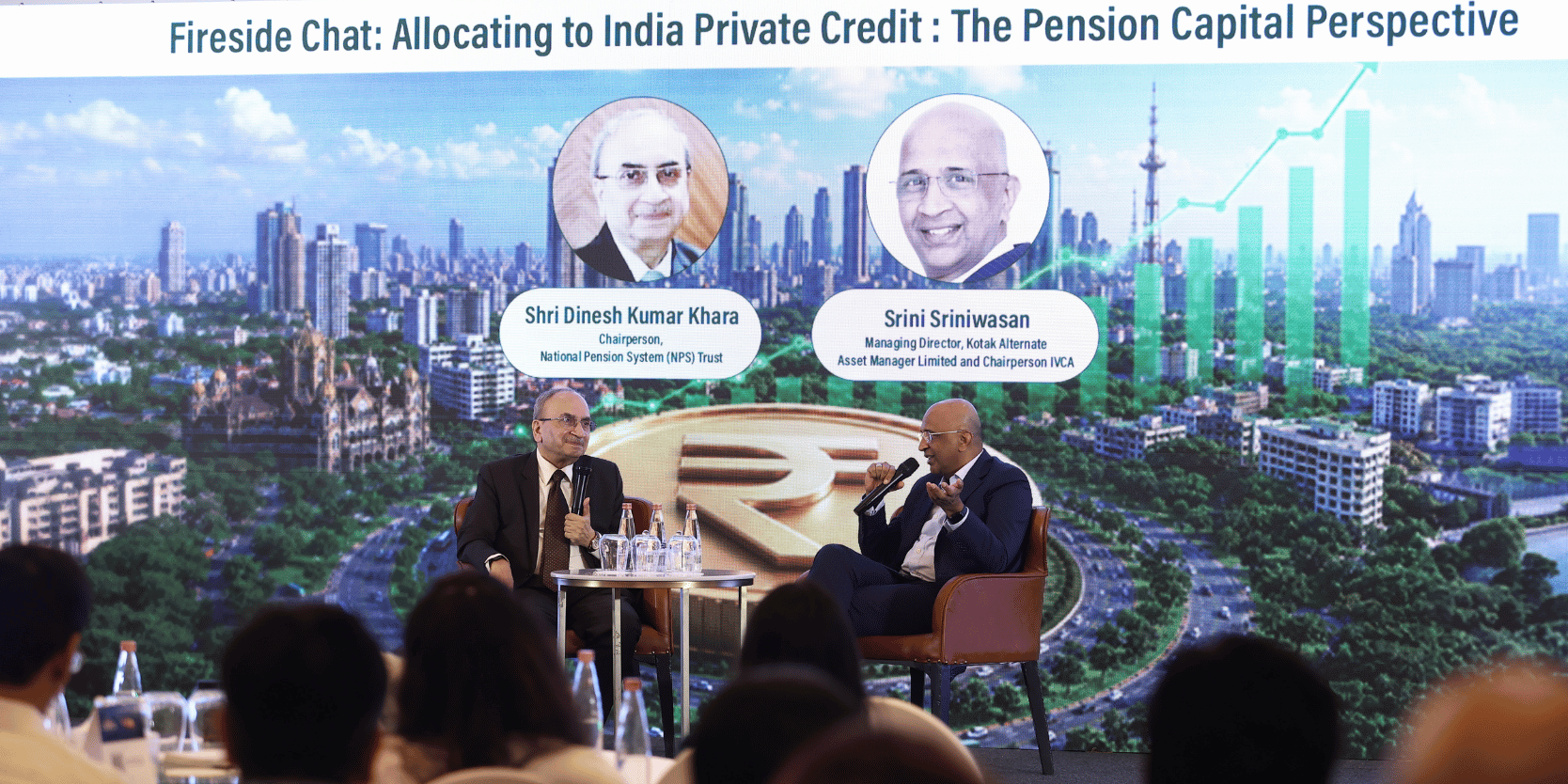

Karthik Athreya, Managing Director, Sundaram Alternates; Rahul Shah, Partner, EvolutionX Debt Capital; and Sandeep Adukia, Senior Managing Partner, Ascertis...

The three film digital campaign highlights weddings, travel and home improvement while showcasing how timely credit can help consumers achieve life goals...

The Bengaluru based company plans to expand scientific research, manufacturing and AI driven hydration solutions after securing growth capital and acquiring...

Suzuki Motor Corporation anchors one of India’s largest impact venture funds to support entrepreneurs across agriculture, healthcare, financial...

Artha Bharat FinMet Physical Gold Fund is the first gold fund authorised by IFSCA in GIFT City, investing in LBMA-standard gold through IIBX with an option for...

Rajesh Jain, Founder and MD of Netcore, said financial brands need to respond to customer intent at the right moment to avoid losing trust and revenue. Netcore...

Harsh Bhatt, Co Founder and CEO of Tulon Materials, said the funding will support IP growth, commercial validation and specialty chemical applications across...

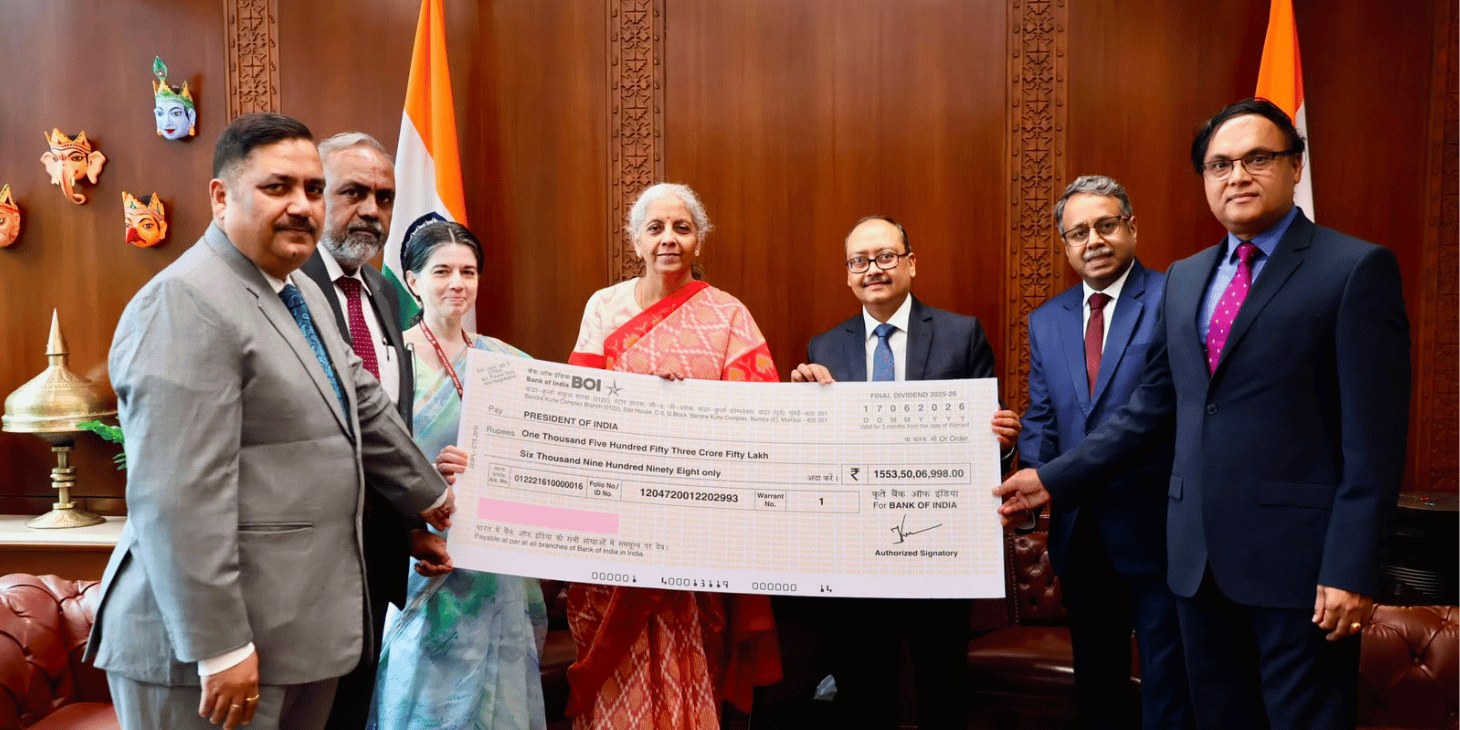

Rajneesh Karnatak, Managing Director and CEO of Bank of India, presented the dividend cheque to Finance Minister Nirmala Sitharaman after the bank reported...

Atul Sood, Senior Vice President, Sales and Marketing at Kia India, said demand for the new Seltos, Sonet, Carens Clavis and MY26 Syros supported the company’s...

Vipin Prakash Mangal, Chairman and Executive Director of Mangalam Global Enterprise Limited, said the launch reflects the company’s move into preventive...

Ashutosh Gupta, Director of Sales and Marketing, Summercool Home Appliances Ltd., said the 5 acre facility will manufacture washing machines, air coolers...

Sohrab Khushrushahi, Co Founder of The Func. Lab, said the investment will support product innovation, wider distribution and expansion across digital, quick...

Rohit Sharma, COO of AbhiBus, said the decade long association remains central to the platform’s work in making bus travel smarter, safer and more seamless...

[…] Mumbai Suburban, Saurabh Katiyar, held a joint meeting with representatives from the real estate sector to address long standing procedural and revenue related challenges. The meeting took place […]